Login

Use LinkedIn or an email

Signup for free

Use LinkedIn or an email

Reset password

Enter email to reset password

Accounting helps companies, investors, regulators and others to describe the financial performance of an entity in a standardised way. Accounting standards provide preparers of financial statements with a set of rules when preparing an entity’s accounts, ensuring this standardisation across the market. Companies listed on public stock exchanges are legally required to publish financial statements in accordance with the relevant accounting standards.

The International Financial Reporting Standards (IFRS) is a single set of accounting standards, developed and maintained by the International Accounting Standards Board (IASB) with the intention of a global consistency – by already developed, emerging and developing economies – providing investors and other users of financial statements with the ability to compare the financial performance of publicly listed companies on a like-for-like basis with their international peers.

The IASB is the standard-setting body of the IFRS Foundation – a public-interest organisation with award-winning levels of transparency and stakeholder participation. Its 150 London-based staff complement hails from almost 30 different countries. The IASB’s 14-member Board is appointed and overseen by 22 trustees from around the world, who are in turn accountable to a monitoring board of public authorities.

More than 100 countries have now mandated the use of the IFRS. These countries include the European Union and more than two-thirds of the Group of Twenty (G20). The G20 and other international organisations have consistently supported the work of the IASB and its mission to implement global accounting standards.

Access the standards here www.ifrs.org

The IFRS for SMEs is a separate International Financial Reporting Standard that is intended to apply to the general purpose financial statements of companies that are typically small and medium-sized entities (SMEs), private entities, and non-publicly accountable entities. Entities that prepare financial statements (referred to as “general purpose financial statements”) for external users should consider whether they should or may apply the IFRS for SMEs in preparing such financial statements. These external users include owners who are not involved in managing the business, The South African Revenue Service (SARS), banks, employees, other lenders, etc.

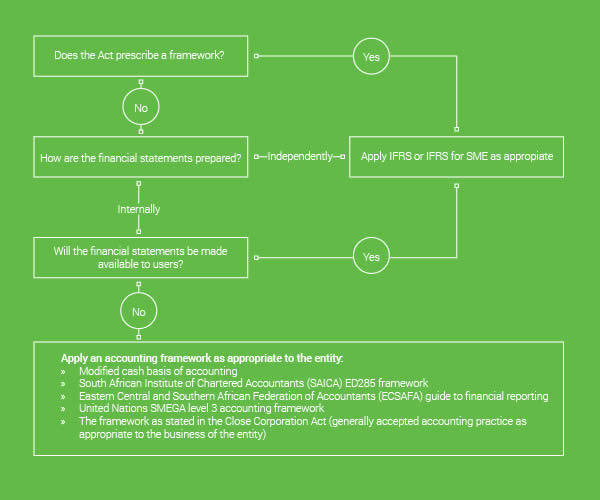

Some entities, such as companies or close corporations, may be legally compelled to apply the IFRS for SMEs. In terms of the Companies Act and Regulations, these entities should determine its “public interest score” and, based on this (considering various tiers) and whether the financial statements are independently or internally compiled, they should or may apply the IFRS for SMEs. (Refer to section 29 of the Companies Act and section 26 and 27 of the Regulations for detail in this regard.)

Other entities such as non-profit organisations, non-governmental organisations, trusts, etc should consider whether there are any legal requirements that compel them to apply a formal financial reporting framework (such as the IFRS for SMEs). An entity’s own memorandum of incorporation, constitution or any other founding document may also require an entity to comply with a formal financial reporting standard. Furthermore, a regulatory body, where applicable, may also prescribe a formal reporting framework to be applied.

To be able to apply the IFRS for SMEs an entity should ensure that it complies with the following definition of a SME (as defined by the IFRS for SMEs), which states that SMEs are entities that:

- Do not have public accountability

- Publish general purpose financial statements for external users

An entity has public accountability (as defined by the IFRS for SMEs) if:

- Its debt or equity instruments are traded in a public market or it is in the process of issuing such instruments for trading in a public market

- It holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses

(Refer to Section 1 of the IFRS for SMEs for more detail in this regard.) Those managing an entity remain responsible for the financial statements of that entity. Management should therefore carefully consider whether the entity should or may apply the IFRS for SMEs.

Access the IFRS for SMEs here: www.ifrs.org

The modified cash basis of accounting uses elements from both the cash basis and accrual basis of accounting. Under the cash basis, you recognise a transaction when there is either incoming cash or outgoing cash. Thus, the receipt of cash from a customer triggers the recordation of revenue, while the payment of a supplier triggers the recordation of an asset or expense. Under the accrual basis, you record revenue when it is earned and expenses when they are incurred, irrespective of any changes in cash.

The modified cash basis is not allowed under Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). This means that a business using this basis must alter the recordation of those elements of its transactions that were recorded under the cash basis, so that they are now accrual basis transactions. Otherwise, an outside auditor will not sign off on its financial statements. However, these changes are fewer than what would be required if a business were to make a full transition from the cash basis to the accrual basis of accounting.

Conversely, the modified cash basis may be acceptable as long as there is no need for the financial statements to be compliant with GAAP or IFRS. This may be the case if the financial statements are only to be used internally – this situation most commonly arises when a business is privately held and has no need for financing.